“I don’t need another dashboard. I need one number I can defend to an auditor with a straight face.”

That was the CFO at a mid-market lender we’ve done work with over the years. It was six weeks after her team had finished building a new executive reporting view. The dashboard was clean. Real-time. Color-coded. And she still couldn’t answer the only question that mattered: When the examiner pulls this delinquency number from the system, will it match the one I just showed the board?

She wasn’t asking for speed. She was asking for defensibility. Those are not the same problem, and most institutions spend their money solving the wrong one.

The reflex that doesn’t fix anything

When an executive stops trusting the numbers, the first instinct is to buy a better way to look at them. Another BI tool. A cleaner dashboard. A faster refresh. It feels like progress, because you can often see the result on a screen by Friday.

But a dashboard is a window. It shows you what’s already in the room. If three teams walk in with three different numbers for the same metric, a prettier window doesn’t reconcile them. It just renders the disagreement in higher resolution.

The reconciliation tax

Here’s what that disagreement costs before anyone even argues about it.

In banks, more than 90% of data users say the data they need is often unavailable or takes too long to retrieve, and 81% call data quality a top challenge (Deloitte, 2024 Banking and Capital Markets Data and Analytics Market Survey). Your analysts live those numbers every day. They burn hours cleaning and reconciling data instead of analyzing it, so at a mid-market shop, whole days a week go to confirming numbers rather than moving them.

That’s the tax you pay for not owning your definitions. And it’s a tax, not a one-time cost. You pay it every reporting cycle, every board meeting, every exam.

How to tell if you actually own a number

Ask four questions about any metric in a board or compliance report:

- Which system holds the source data?

- Where is the calculation logic applied?

- Which definition is authoritative?

- Who approves a change to it?

If you can’t answer all four, the metric already exists in more than one version. It doesn’t matter how clean the dashboard looks. The visualization layer was never the bottleneck. The definition layer is.

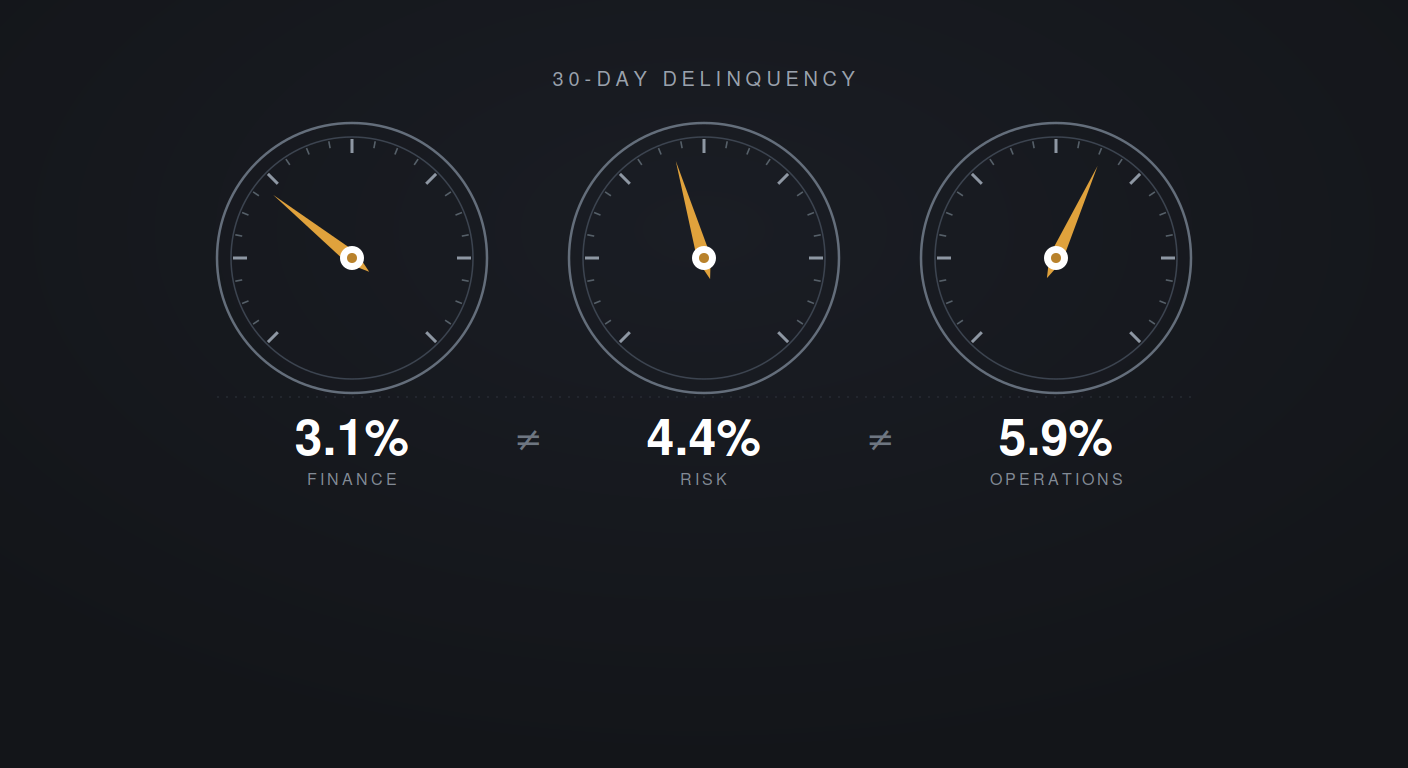

This is the part that catches people off guard. They assume the problem is technical, a tooling gap. It’s almost always a definition gap. Nobody wrote down what “30-day delinquency” includes and excludes, which system is the source of record, and who’s allowed to change it. So Finance, Risk, and Operations each made a reasonable assumption, and now you have three numbers and a steering committee that opens every meeting by arguing about whose data is right.

Why this is now a finding, not just an annoyance

For a while you could live with that. Expensive and irritating, but survivable. That window is closing.

For years the OCC has told bank directors to treat a breakdown in reconciliations, the checks that confirm the bank’s own records agree with each other, as a red flag in the reports they’re handed. Translation: The number your CFO shows the board and the number the auditor pulls from the system are supposed to match. When they don’t, that gap isn’t an internal inconvenience. It’s a finding waiting to happen.

The governance bar is rising too, and it’s drifting down-market. BCBS 239, the risk data aggregation and reporting principles the Basel Committee wrote after the 2008 crisis, was aimed at the biggest banks. But it has become the template for what regulators treat as good, and US supervisors are steadily pushing the same data-governance expectations toward regional and mid-market institutions.

The principles are blunt about what good looks like: data aggregated automatically rather than stitched together by hand, accurate under stress, and consolidated into one reliable view. For every metric in a risk or compliance report, that means a precise definition, a source system, a named data owner, a named control owner, and a documented path for what happens when the metric breaches a threshold.

Read that list again. A dashboard satisfies none of it. A dashboard without those five things behind it is decoration.

The wrong race

So the race everyone’s running, speed to visualization, is the wrong race. The institution that wins isn’t the one that can spin up 20 views the fastest. It’s the one that can produce a single number and, when an auditor asks, walk the lineage all the way back to the source without breaking a sweat.

One defensible number beats 20 unreconciled ones on demand. Especially in an exam.

What actually solves it

This is the problem GOBLIN was built for. Not another reporting layer stacked on top of the mess, but a governed foundation underneath it. Source data consolidated from your legacy systems into one place. Definitions applied consistently, so Finance, Risk, and Operations are reading from the same book. Lineage you can trace. Access controlled by role. The dashboards come with our normal Risk Support. What makes them defensible is what sits behind them.

PAG’s team has built this for top-tier banks and stood it up for mid-market lenders who needed it running yesterday. The CFO at the top of this post stopped asking for a better dashboard the day she could answer the only question that mattered: Where did this number come from, and can I prove it?

If your teams are still walking into meetings with three numbers for the same metric, that’s the conversation worth having.

David LaRoche is managing partner, U.S. Operations, for Predictive Analytics Group, which helps clients cost-effectively bridge the gap between analysis and impactful strategic or tactical decisions. To learn more about how GOBLIN can consolidate your data environment and accelerate your AI readiness, schedule a discovery call with us. Or you can schedule a no-obligation consultation to discuss how we can help with your defensibility changes.